Business & Equipment Finance Solutions

Finance that moves as fast as your business

When a contract lands, you need the tools to deliver it immediately. We structure agile equipment financing that gets your machinery on-site faster, simplifying the application process to ensure you meet your project timelines.

From expanding your heavy vehicle fleet to securing essential business equipment loans, we access lenders who value the asset itself to help secure your gear while preserving your working capital.

Partnering with specialised lenders to deliver fast, cash-flow-friendly solutions

Your operations — fully funded

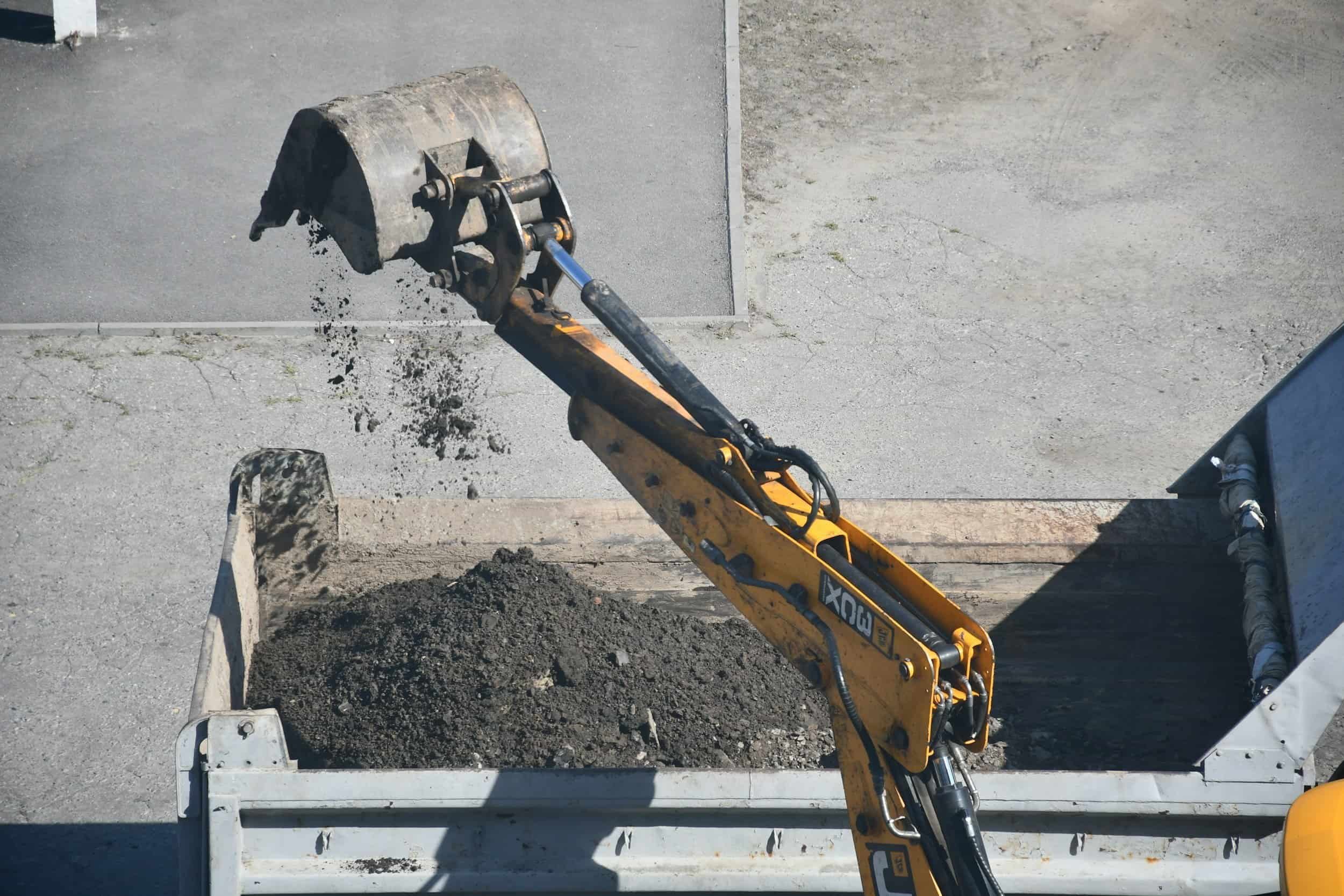

For earthmoving, civil, and industrial plant, we structure facilities with or without presale, leveraging the asset's value to often secure 100% finance with no deposit.

Plant & Machinery

From single prime movers to entire fleet upgrades, we provide tailored financing for trucks, trailers, and light vehicles, to grow your capacity in line with your contracts.

Fleet & Logistics

Access fast, unsecured business loans to bridge cashflow gaps, purchase inventory, or fund expansion. Keep your business agile without needing to use real estate as security.

Cashflow & Working Capital

Specialist funding to clear ATO tax arrears. We structure facilities that pay out the debt directly, allowing you to normalise your tax standing and focus on running the business.

ATO & Tax Obligations

Funding based on trading strength

Fast-growing businesses often have complex balance sheets. A cashflow dip or a pending tax bill shouldn't prevent you from securing the assets you need to grow.

We access specialised lenders who look beyond the checkboxes. By leveraging the value of your machinery or your monthly revenue, we provide capital solutions that solve working capital gaps and ATO debt hurdles.

Aligned with Queensland’s infrastructure pipeline.

From the Brisbane Olympic infrastructure to resource extraction in the Basin, we know the contracts that underpin asset values, and use local market intelligence to mitigate lender risk.

We prove to banks that your new machinery is backed by secure, long-term workflow in high-demand corridors, ensuring you get approved where others might hesitate.

Core Markets: Sunshine Coast • Brisbane • Gold Coast • Regional QLD

Case study

Funding a complex $3M offshore mining asset

Challenge:

To fulfil a major contract, a mining client needed to acquire $3M in specialised equipment from South America. Standard lenders rejected the deal because the asset was used, located offshore, and required a 6-month custom build, carrying prohibitive construction and foreign exchange risks.

Strategy:

Rather than trying to force this into a standard equipment loan, we treated the transaction like a capital project. We structured a multi-phase funding solution aligned directly to the asset's milestones. We negotiated with specialist lenders, addressed the FX exposure, and structured the facility to actively protect the client's cash flow during the long 6-month construction phase.

Outcome:

The $3M was secured, ensuring the smooth acquisition, shipping, and commissioning of the equipment with zero disruption to the client's daily operations. Most importantly, delivering this initial project proved their capability, which opened the door for the client to win several more large-scale contracts shortly after.

Business & Equipment Finance Common Questions

-

Yes, it is often possible. Many commercial lenders offer streamlined equipment finance policies that do not require full financial statements or tax returns. Provided your business has been trading for 12 to 24 months and holds an active ABN and GST registration, we can typically structure and secure funding based on your trading history and the strength of the asset itself.

-

Yes. Unlike major banks that freeze lending when they see tax arrears, we access specialised lenders who look at your current trading strength. We can often structure equipment financing that secures the asset you need, or even refinance existing fleet equity to pay out your ATO debt.

-

Yes. While major banks permit private vendor and auction sales, their rigid processes can take weeks, causing you to miss out on the asset. We partner with agile funders who operate in days, not weeks. We manage the fast-tracked payout process so you secure the gear immediately.

-

While standard banks typically restrict lending to "easy" or standard assets like vehicles, we can fund almost anything your operations require. We structure finance for complex requirements including aircraft, marine vessels, yellow gear, farm machinery, manufacturing plants, IT hardware, and SaaS licences.